ADUs Are Now Legal Statewide

An ADU is Now Legal By Right

(617) 913-3237

Real Estate Company

Closing Day Guide for Massachusetts Homebuyers

Closing day is when your new home officially becomes yours — but it’s also a process filled with critical steps, paperwork, and timing. This guide breaks down exactly what to expect on closing day in Massachusetts so you can move forward with confidence.

Closing day is the final step in your home purchase journey – an exciting and sometimes nerve-wracking occasion when you officially become a homeowner. For Massachusetts homebuyers, including first-time buyers, move-up buyers, and downsizers, it’s important to know what to expect on closing day.

This guide provides a detailed, step-by-step look at the closing day timeline, the roles of all parties involved, how the final walk-through works, typical closing costs, documentation you’ll need, and common mistakes to avoid. With this knowledge, you can approach closing day with confidence and ensure a smooth, successful transaction.

Closing day in Massachusetts typically unfolds in a series of steps leading up to the transfer of ownership. Here’s a general timeline of what happens on closing day :

The final walk-through is a crucial step for buyers on closing day. This walkthrough typically takes place either the day of closing (just a few hours before the signing) or one to two days prior. Its purpose is to give the buyer a last opportunity to inspect the property and verify that everything is in order as expected. Here’s what to look for and expect during a final walk-through:

Remember, a thorough final walk-through is for your protection. Skipping it or doing it hastily would be a mistake. Take your time and be observant. Use a checklist if necessary to ensure you inspect all areas. If all looks good, you can proceed to the closing table with peace of mind.

A successful closing involves coordination between several parties. In Massachusetts, you can expect to encounter the following people on or around closing day and understand their roles:

Understanding everyone’s role can make the process less intimidating. Don’t hesitate to ask questions on closing day – the professionals present (attorney, agents) are there to guide you through the process.

Sitting down at the closing table is the moment where all the preparation and paperwork come together. Here’s what to expect at closing day as a buyer in Massachusetts:

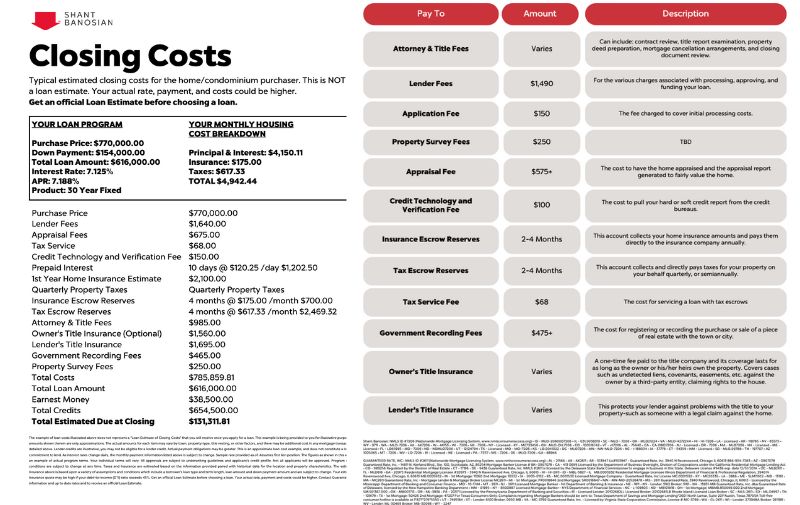

Closing costs are the various fees and prepaid expenses due at the completion of a real estate transaction. In Massachusetts, homebuyers should budget roughly 2% to 5% of the purchase price for closing costs (on top of the down payment). The exact amount will vary based on your loan, the home price, and other factors. Here are typical closing costs for buyers in Massachusetts and what they cover:

Tip: A few days before closing, you should receive your finalized Closing Disclosure from the lender which lists all of your closing costs line by line. Review it carefully and ask questions about anything you don’t understand or didn’t expect. There should be no big surprises on closing day, because you have the right to see these figures in advance. If something looks off, have your loan officer or attorney clarify it prior to the closing meeting.

To avoid any last-minute issues on closing day, make sure you come prepared with all necessary documentation and items. Here’s a checklist of what buyers need to bring or have ready at the closing in Massachusetts:

By preparing all the required documents and funds ahead of time, you can avoid delays on closing day. Your real estate agent and attorney will usually provide a pre-closing checklist to ensure you have everything in order. Double-check that list the night before closing so you can arrive with confidence that nothing is missing.

Closing day can be complex, and mistakes or last-minute surprises can derail an otherwise smooth transaction. Here are some common mistakes buyers should avoid on or before closing day:

By avoiding these common pitfalls, you can greatly reduce stress and ensure your closing day goes as smoothly as possible. The key is preparation, communication, and attention to detail. Real estate professionals in Massachusetts handle closings every day, so lean on their experience and don’t hesitate to ask for guidance if something is unclear.

You did it — congratulations on becoming a homeowner! Closing day is no small milestone, and now that the paperwork is signed and the keys are in hand, it’s time to take a deep breath and celebrate. Whether this is your first home or your next chapter, you’ve successfully navigated one of the most important moments in your real estate journey.

Closing day is when you officially take ownership of your new home. You'll review and sign final documents, pay any remaining closing costs, and once everything is signed and recorded, you’ll receive the keys. The process typically takes about an hour and is often held at your attorney’s office or a lender-approved location.

Yes. Bring a valid government-issued photo ID, proof of homeowners insurance, and a cashier’s check or wire confirmation for your closing funds. It’s also helpful to bring your Closing Disclosure and checkbook in case of small last-minute adjustments.

You’ll receive the keys once the deed has been recorded at the Registry of Deeds. If your closing happens in the morning, recording usually occurs the same day. Once confirmed, you’ll be given the keys and can officially move in.

The final walk-through is your last chance to ensure the property is in the agreed-upon condition, and I strongly recommend doing it the morning of closing to catch any last-minute issues — like a leaking toilet, broken appliance, or HVAC failure — before ownership officially transfers. Doing it too early can leave you vulnerable to problems that arise between the walkthrough and closing.

Delays can happen due to funding issues, missing documents, or last-minute walk-through problems. Stay in close contact with your attorney and agent. Most issues can be resolved quickly, but serious problems may require rescheduling the closing or creating a temporary agreement.

ADUs Are Now Legal Statewide

An ADU is Now Legal By Right

Have Repairs Done Before You Sell With No Cost

Borrow With No Interest Loan To Have Repairs Done & Pay At Closing

Home Selling Options

With Us You Have Many Options. Learn About Them

Massachusetts Smoke and CO Requirements

Smoke and Carbon Monoxide Detector Requirements in Massachusetts

Read the Massachusetts Guide

Read the Guide to Massachusetts Smoke and Carbon Monoxide Requirements When Selling

Have questions before or after closing? We’re here to help you finish strong — and support you beyond the final signature.